There exist many ways to calculate depreciation, usually depending on the type of assets and how fast their value decreases. The declining balance is one of the depreciation methods that companies can use to depreciate assets and it’s a common practice. In this article, we will be explaining the declining balance depreciation method and provide an example so that you can clearly understand how it works. As seen in the formula of declining balance depreciation above, the company needs the deprecation rate in order to calculate the depreciation. Hence, it is important for the management of the company to determine the depreciation rate that can allow the company to properly allocate the cost of the fixed asset over its useful life.

Example 3: Double-Declining Depreciation in Last Period

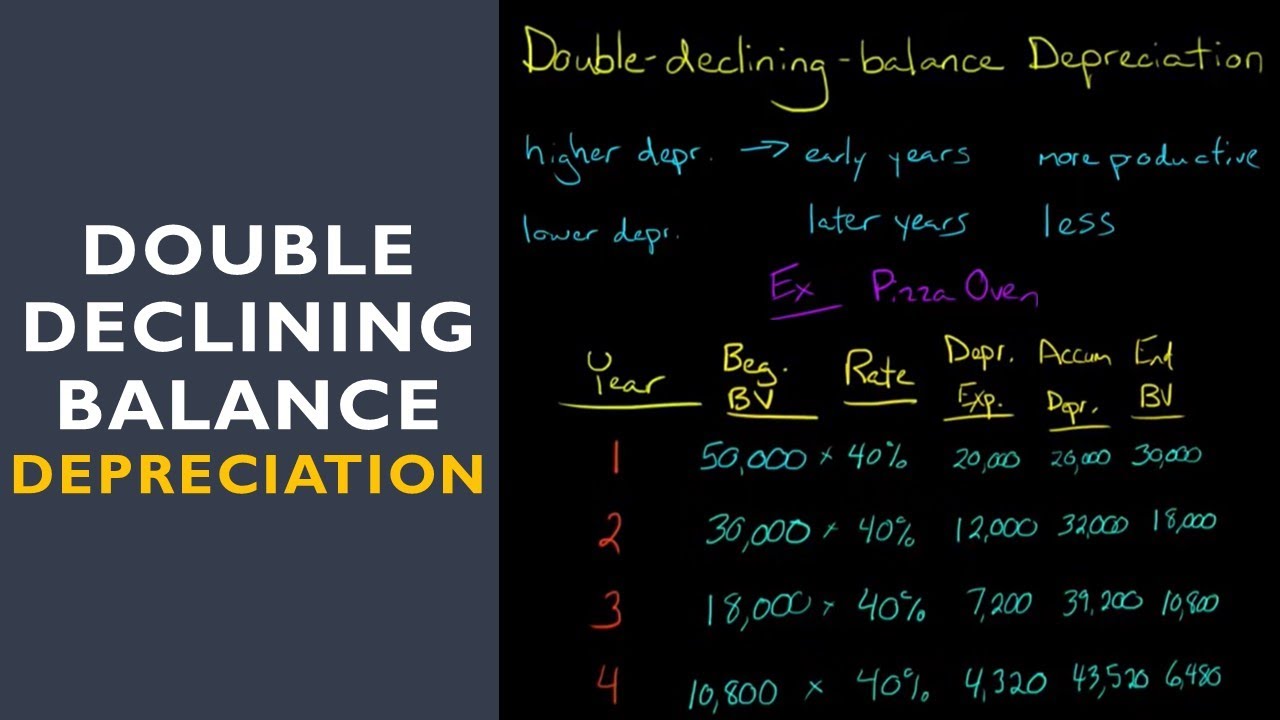

CCC purchased new machinery for the construction business at a cost of $50,000 with a salvage value of $4,000. Based on past experience, the same type of machinery has a useful life of 8 years and is depreciated at a rate of 15%. When applying the double-declining balance method, the asset’s residual value is not initially subtracted from the asset’s acquisition cost to arrive at a depreciable cost. The declining balance technique represents the opposite of the straight-line depreciation method which is more suitable for assets whose book value drops at a steady rate throughout their useful lives. Employing the accelerated depreciation technique means there will be lesser taxable income in the earlier years of an asset’s life.

What is the declining balance method of assets depreciation?

Management that routinely keeps book value consistently lower than market value might also be doing other types of manipulation over time to massage the company’s results. Suppose that the company changes salvage value from $10,000 to $17,000 after three years, but keeps the original 10-year lifetime. With a book value of $73,000, there is now only $56,000 left to depreciate over seven years, or $8,000 per year. That boosts income by $1,000 while making the balance sheet stronger by the same amount each year. The second scenario that could occur is that the company really wants the new trailer, and is willing to sell the old one for only $65,000. In addition, there is a loss of $8,000 recorded on the income statement because only $65,000 was received for the old trailer when its book value was $73,000.

What are the Chart of Accounts in Accounting? (Simple)

Instead, we simply keep deducting depreciation until we reach the salvage value. As you can see from the above example, depreciation expense under reducing balance method progressively declines over the asset’s useful life. This is a good method to be used for assets that lose their value mostly in the earlier years of their expected useful life. Products like computers, cars or anything technological would be good candidates for the declining balance depreciation. Under the declining balance methods, the asset’s salvage value is used as the minimum book value; the total lifetime depreciation is thus the same as under the other methods.

Although any rate can be used, the straight-line rate is commonly used as a base to determine the depreciation rate for the declining balance method. This is due to the straight-line rate can be easily determined through the estimated useful life of the fixed asset. The company can calculate declining balance depreciation for fixed assets with the formula of the net book value of fixed assets multiplying with the depreciation rate. In general, the company should allocate the cost of fixed assets based on the benefits that the company receives from them.

- An asset costing $20,000 has estimated useful life of 5 years and salvage value of $4,500.

- To calculate the first-year depreciation, we just need to deduct the salvage value from the value of the book of the asset.

- Under the declining balance method, depreciation is charged on the book value of the asset and the amount of depreciation decreases every year.

- To use the template above, all you need to do is modify the cells in blue, and Excel will automatically generate a depreciation schedule for you.

- That’s why depreciation expense is lower in the later years because of the fixed asset’s decreased efficiency and high maintenance cost.

With declining balance methods of depreciation, when the asset has a salvage value, the ending Net Book Value should be the salvage value. Under Straight Line Depreciation, we first subtracted the salvage value before figuring depreciation. With declining balance methods, we don’t subtract that from the calculation. What that means is we are only depreciating the asset to its salvage value.

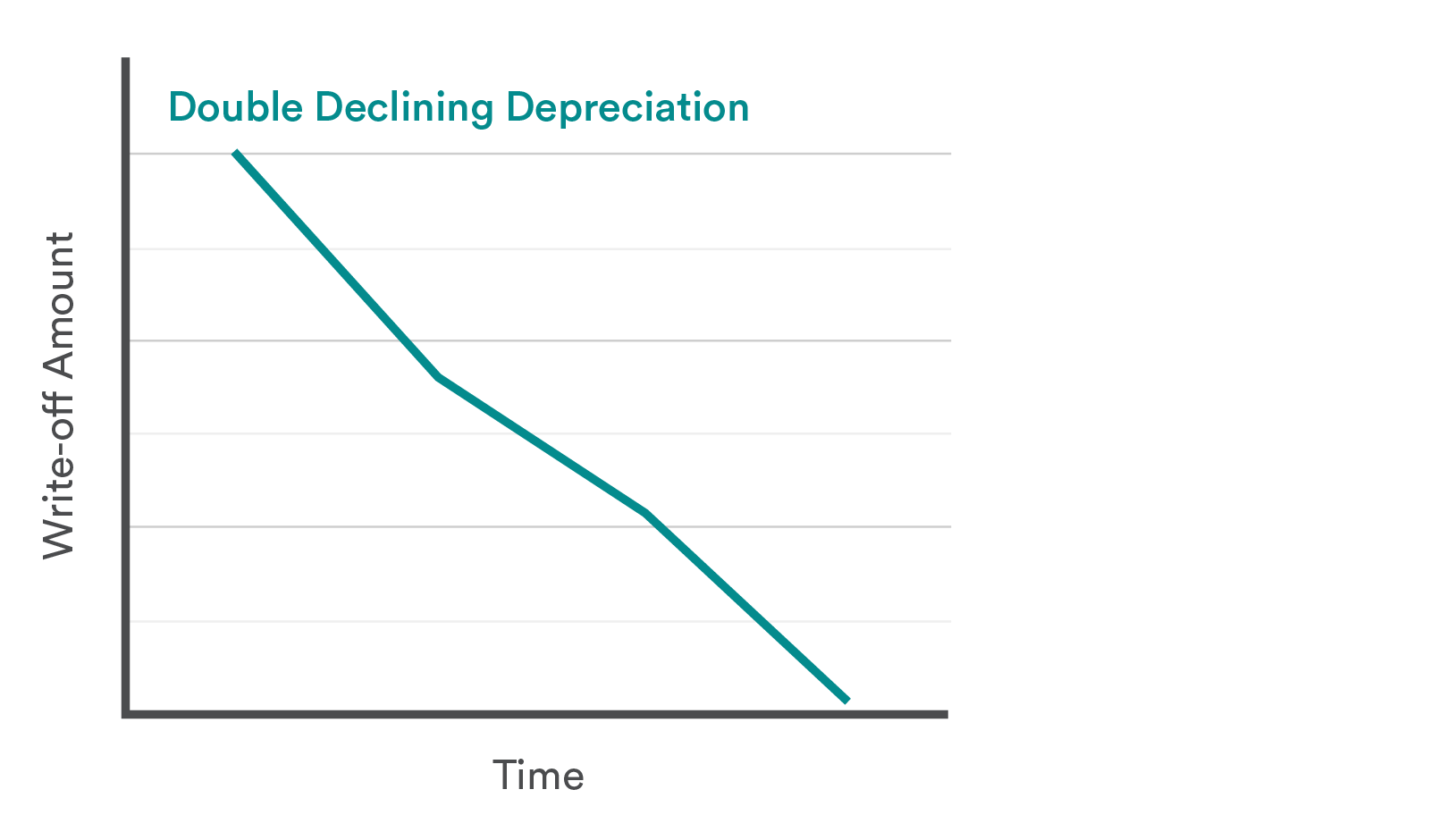

The double declining balance method of depreciation reports higher depreciation charges in earlier years than in later years. The higher depreciation in earlier years matches the fixed asset’s ability to perform at optimum efficiency, while lower depreciation in later years matches higher maintenance costs. It’s ideal to have accounting software that can calculate depreciation automatically.

GAAP is a set of rules that includes the details, complexities, and legalities of business and corporate accounting. GAAP guidelines highlight several separate, allowable methods of depreciation that accounting professionals may use. A more common depreciation method is the straight-line method, where the depreciation expense to be recognized is spread evenly over the useful life of the underlying asset. This method is the simplest to calculate, and generally represents the actual usage of assets over time. It is also more likely to leave carrying values on the balance sheet that reflect the remaining market values of assets (though there is not necessarily a direct relationship between carrying value and market value). Depreciation is an accounting process by which a company allocates an asset’s cost throughout its useful life.

Instead of multiplying by our fixed rate, we’ll link the end-of-period balance in Year 5 to our salvage value assumption. However, one can see that the amount of expense to charge is a function of the assumptions made about both the asset’s lifetime and what it might be worth at the end of that lifetime. direct cost vs indirect cost cost accounting Those assumptions affect both the net income and the book value of the asset. Further, they have an impact on earnings if the asset is ever sold, either for a gain or a loss when compared to its book value. He has a CPA license in the Philippines and a BS in Accountancy graduate at Silliman University.

Reducing balance method causes reported profits of a company to decline by a higher depreciation charge in the early years of an assets life. This method often is used if an asset is expected to lose greater value or have greater utility in earlier years. Some companies may use the double-declining balance equation for more aggressive depreciation and early expense management. 150% declining balance depreciation is calculated in the same manner as is double-declining-balance depreciation, except that the rate is 150% of the straight-line rate.